It seems appropriate to begin the first post breaking my long hiatus with a post about virtual entities being in Singapore whilst not being in Singapore. Hello! I’m still here! But where is here? I’m not in Singapore, but soon I will be. At times my location almost seems arbitrary; I am neither here nor there, but I’m online, which may as well be everywhere.

After a grueling 2015 and returning to London, I shrank away from the relentless public exhortations of social media, grew unreasonably incensed at the constant burden of interactivity, and even began a series of (incomplete) writing on my hatred for infinite scroll and other modern scourges of online interactivity. The benefit of withdrawing myself from the clatter of social media was that I found time to teach myself how to use tools like Unity, three.js, Blender and Meshmixer… so there’ll be more on those in upcoming posts…

But now! I recently read this page by Ghost Foundation moving to Singapore. The article sounds like it must be related to Singapore, but it is really not about Singapore. Singapore may as well not exist, except on paper as some almost-mythical stable benevolent friendly-tax offshore island. Ghost makes no real impact on Singapore by having been incorporated in Singapore, for it is merely a virtual marriage-of-convenience. I found it funny to see it was even reported as news by Channel News Asia (what passes muster for “news” in these parts… zzzz), and a little funny to read comments from Singaporeans getting excited and “welcoming” them to Singapore, when they have clearly stated on their post that they won’t be in Singapore (and therefore their virtual presence does not contribute directly to the tech startup scene in Singapore). They say they’re not doing it for tax avoidance but it basically sounds like tax obfuscation to me!

VAT rules however do seem completely obscure and confusing to consumers and small businesses owners/startups. I briefly entertained the thought of incorporating myself as a business in the UK the same way DBBD is registered as a company in Singapore (as a designer and builder of various curious interactive things). But after reading up on the VAT MOSS situation, it makes absolutely no sense to do so. I’m not even sure how many small business owners know about this.

VAT MOSS (Mini One-Stop Shop) was rolled out on 1 Jan 2015. This means now if a small/micro-business wants to sell an electronically supplied service (eg: electronic download, software update) to a consumer (non-business customer) within the EU, it needs to charge VAT at the rate applicable in the consumer’s location and remit this on quarterly returns via MOSS.

Yes, MOSS is the real name, so cue the GATHERING NO MOSS jokes and #VATMESS. They’ve named it MINI ONE STOP SHOP. With such a ridiculous name, it makes me feel as if the person who named it probably thinks the internet is a series of tubes and that you just press a button to turn on the tubes.

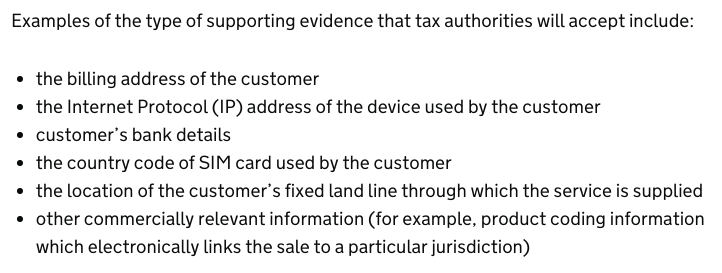

The implication is that small companies which may not have reached the taxable threshold are going to go from not paying VAT to filing for VAT MOSS 4 TIMES A YEAR all of a sudden, and are expected to collect a host of personal information from all its customers in order to determine which ones are from one of the 28 countries in the EU, and then they need to magically manage to apply the correct VAT rate to the purchase (there are apparently 81 different VAT rates??). And if that is not confusing enough, the proof of customer location (personally identifiable information) and must be securely (??) stored for 10 years by the company which is also required to register as a data controller (£35/year). (Additionally, not registered as a data controller when required to is a criminal offence… a provisionary glance I took at the ICO site suggests that the fine could be up to 5000 euros)

(For more facts see: EU VAT ACTION)

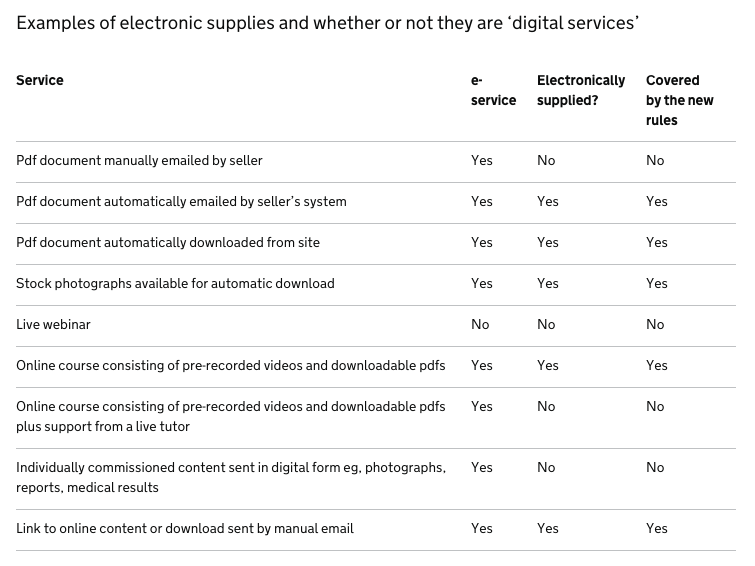

The key term here seems to be ‘electronically supplied’ as opposed to having “human intervention”. The European Commission’s explanatory notes (Annex on Page 86) writes:

‘Electronically supplied services’ as referred to in Directive 2006/112/EC shall include services which are delivered over the Internet or an electronic network and the nature of which renders their supply essentially automated and involving minimal human intervention, and impossible to ensure in the absence of information technology.

From HMRC: VAT MOSS – So apparently if you “manually” attach a PDF, it is not covered under VAT MOSS. But if you “manually email” an upload link, it’s covered under VAT MOSS?? Looks like these people have never attached a document and found it too big so you have to upload it elsewhere and send someone a link.

The directive which the definition is taken from is from 2006. How seriously outdated is that? In the last 8 years, a lot has changed about the internet, and the range of electronic products and services offered. To put things into context, I first started learning programming 7 years ago and in those 7 years in my role as an interactive designer/developer all the technologies have changed, the modes of distributing information have completely changed, internet selling/services have totally changed.

VAT MOSS rules currently lack a nuanced understanding of how quickly the internet changes and grows, and this is causing senseless confusion because there is no logical line on what constitutes sufficient human intervention in a lot of new scenarios that are emerging.

To me this sounds a lot like this:

Who wrote the rules for VAT MOSS? What are their credentials, or interests, and do they know anything about how the internet works today??? Human intervention is a stupid criteria in small digital businesses where people ought to be working smart and automating processes even at the smallest level. Were the views of online businesses represented in the discussion, or at least to provide the commission with an adequate understanding of the likely future of electronic businesses? And how on earth do you draw the line on what constitutes sufficient human intervention? There is really no difference if I do it or I script up something which automatically sends that email on my behalf. Is my human intervention as author of the automated script not counted?? I still wrote the script, letter by letter, intervening with the letters on my keyboard.

Another question that came to mind was – HOW MANY PEOPLE ARE PAYING THROUGH VAT MOSS? Surely all the companies worth taxing are already taxed normally for being over the threshold. I’d like to find out, what amount of VAT MOSS is actually being paid from the small/micro businesses who are now newly affected from the 1 Jan 2015 ruling for the first time?

The Internet has many stories of people paying ridiculously exorbitant amounts in accounting software and services only to find out they have to pay insultingly low VAT on their digital business.

Just filed my first #VATMOSS return with @HMRCgovuk – cost me GBP700+ in software and accounting to calculate that I owed 18.74— Cory Doctorow (@doctorow) April 14, 2015

So if the VAT being collected is so insultingly miniscule for many individuals and incurring so much unnecessary administrative problems and additional business expenditure, the question is – was it really worth implementing? If the goal was to target big companies like Amazon, why is the fallout affecting small businesses and forcing them out of business (and correspondingly, pushing customers towards the big companies). If this is all a matter of proving success of a scheme by numbers, then how much VAT in total is actually being paid between UK and EU countries on digital business under VATMOSS since 2015?

This is where UK’s FOIA sounds like some black voodoo magic to a Singaporean like me – almost unbelievably it is a land where you can ask for information and public authorities are legally required to give a proper reply! (How sad that I have to be so excited about this…) A quick gander on whatdotheyknow.com brings up user john_117’s fascinating FOI correspondences with HMRC. It reveals that since it is collected quarterly, in john_117 first correspondence in March they didn’t have the data yet, but then in July they make a turnaround by mentioning that “Under section 22(1) of the FOIA, we are not required to provide information in response to a request if we intend to publish the information in the future” and that they won’t be providing a country-by-country breakdown so as not to “prejudice relations between the UK and other Member States” by “disclosing tax revenues of other Member States”.

It is now 2016 and searching the gov.uk site does not turn up any publication of statistics. A little disappointing. Perhaps I just don’t know where to search.

More disturbingly, I tried to find what panel or commission was responsible for making decisions on VAT MOSS, but so far haven’t figured it out. The question I wonder is: in the process of making these decisions, did they include anyone or any groups representing the interests of small digital businesses which will be affected by VAT MOSS?

The only way out of VAT MOSS seems to be to block all EU buyers or (virtually) move out of EU. Or use VAT MOSS and raise all your prices by 20% or more to include VAT (or allow it to cut significantly into your own profits), collect at least two of the following information from each your customers and securely store it for 10 years:

EVEN THOUGH ACTUALLY ALL YOU WANT TO DO IS SELL ONE TINY KNITTING PATTERN ONLINE

Don’t even get me started about the potential complications when you have to deal with people with foreign billing addresses who spend equal parts of time in more than one country. I realised recently that I wasn’t charged VAT for an digital service which I use in both Singapore and London – a scenario that seems to be in a grey area. I paid for the digital service with a credit card registered to a Singaporean bank with a Singapore billing address and the printed matter was to be mailed to my Singapore billing address – but I physically reside in London and my order would have come from a IP address in UK – and I use only a +44 UK phone number. The unnamed supplier in this case obviously had to made a blanket presumption on my location based on billing address and bank address, rather than IP address or SIM address. But this really shouldn’t be made into a confusing guessing game for business owners.

In 2016 they released some half-baked simplification, citing that business owners are allowed to exercise their best judgement. How on earth can one exercise their best judgement on what appears to be a poorly thought out scheme?

From HMRC: “There is no registration threshold on cross border supplies of services and businesses of all sizes fall within the scope of the changes. However, this only applies where supplies are made in the course or furtherance of a business. If activity is carried out as a hobby (ie only on a minimal and occasional basis), HMRC does not normally see this as a business activity for VAT purposes. HMRC’s analysis of the VAT MOSS returns submitted by UK businesses so far indicate that some of those registered for VAT MOSS may not be in business for VAT purposes.

HMRC will contact those already registered for VAT MOSS whose returns suggest they may not be in business.”

OH NO, IS MY BUSINESS A LIE? IS MY ENTIRE PRACTICE ACTUALLY ONE BIG NON-TAXABLE HOBBY?? And by extension, are they saying that online sales doesn’t need to be declared as income tax? Or not? Or what? What a confusing message to send to small self-employed business owners.

Creating a “level playing field” through #VATMOSS means programming 6,724 possible tax combinations for a $10 sale. https://t.co/V5Lty66H49— Heather Burns (@WebDevLaw) February 17, 2016

Unfortunately, what seems direly shortsighted is that VAT MOSS doesn’t take into account the complexity of international online transactions today. A more updated and intelligently written VAT system is needed to nurture the growth of small and micro digital businesses so that business can be more decentralised and diverse – rather than unfairly taxing even the smallest digital businesses with wildly unrealistic administrative and financial burdens.

But back to the Ghost in Singapore. It is funny that the poorly devised VAT MOSS (which is effectively an injunction against transactions that are virtually mediated) has driven companies to make their operations even more virtual by virtually incorporating in another country.

I wondered where Ghost’s virtual address was, as its not uncommon to see a host of virtual companies sharing the same address in town – you even see the ‘prestigious’ addresses even being advertised at times. It got me thinking how many companies in Singapore use a virtual address – could we find an actual number for how many virtual/ghost companies there are within Singapore, or in Singapore’s CBD?

So I wanted to find a directory of public companies, which led me to ACRA. I also cross checked with data.gov.sg – but it only has a table on taxable companies and which sectors they were in. Global OpenData Index (a great resource) also confirms that ACRA doesn’t make this information available. ACRA mainly allows you to “buy information” rather than to obtain it from them for free. Perhaps I can only access a directory of public companies (and their addresses) if I pay for the data? But looking at it so far, they only allow you to buy individual business profiles for $5.50 (£2.70) a pop, and if I remember it right from when I had to get a copy of my business profile, they just generate a flat page of information trapped inside ancient HTML tables – rather than providing you with data in a format that is actually usable.

My circumlocutory search for data ends here for the night, but I’ll continue another time…

Related posts:

Do Digital Worlds Fill up with Digital Kipple?

Do Digital Worlds Fill up with Digital Kipple?

UP Singapore Urban Prototyping Weekend – Postcode Postcard

UP Singapore Urban Prototyping Weekend – Postcode Postcard

A Mini Tour-de-Paris for a Pot of Lavender

A Mini Tour-de-Paris for a Pot of Lavender

Growing Mushrooms, Moss and Lavender – Part II (1 year later)

Growing Mushrooms, Moss and Lavender – Part II (1 year later)

Real Life and Second Life Paredolia

Real Life and Second Life Paredolia

Where were you in ’95? – Finite capacities and data retrieval in physical media formats.

Where were you in ’95? – Finite capacities and data retrieval in physical media formats.

Singapore Art Week 2022: Where to see Debbie’s works

Singapore Art Week 2022: Where to see Debbie’s works

Growing Mushrooms, Moss and Lavender – Part I

Growing Mushrooms, Moss and Lavender – Part I